.png)

Abhishek Upadhyay is the Executive Vice President and Co-Head Economics & Fixed Income Research at ICICI Securities Primary Dealership

July 17, 2026 at 10:35 AM IST

The sharp decline in international crude prices to close to pre-war levels recently has shifted the narrative on RBI monetary policy. Analysts who expected the rate hike process to begin in the June-August meetings have changed those views, and consensus has shifted towards stable policy rates in 2026. That said, swap markets are still pricing in roughly three hikes in the current fiscal year starting in the October MPC meeting, and that still appears more reasonable.

The recent price action in the benchmark Brent crude price, which is up over 20% from the early July lows of $70 a barrel, is a confirmation that geopolitical risk is far from fully resolved. Given the high uncertainty and depleted global inventory levels, the $80-100 a barrel range for crude prices looks reasonable. This range acknowledges that the tail risk of record high crude prices has diminished, but the downside is also likely limited.

If RBI assumes a similar range in its inflation model, then there is only modest scope for downward revision in inflation forecasts, perhaps 20-30 basis points from its 5.1% projection for the year. However, there is a bigger downside to RBI’s forecast of 4.7% core inflation, with a 4-4.5% average more likely (versus 3.9% in June).That view also derives from the bias for softer inflation in the new CPI series, particularly for services inflation categories such as housing, where price pressures look puzzlingly low.

Low Core Vs High Headline

The big question is whether the RBI MPC needs to hike with core inflation undershooting forecasts. Note that once precious metals are also excluded, core inflation was 140 bps lower than the conventional gauge (at 2.5% year on year), and the Governor has often referred to this metric in his public comments. This gap may narrow a bit going ahead, but core ex precious metals may still average closer to 3% rather than 4%.

These benign inflation internals shouldn’t, however, diminish the case for two to three hikes. Here are the reasons.

One, the current level of policy settings is too loose given the inflation-growth mix. Despite the RBI's emphasis on the core ex-precious metals metric, it is not the best metric for measuring underlying inflation in an environment where there is a broad-based rise in food and fuel inflation. If the upturn in food inflation was narrowly based and led by volatile segments such as vegetables, there could be a case to look through the higher inflation. But that is not the case currently, and with rainfall tracking a staggering 23% below the long-period average, there is no case to cherry-pick the softest metric to make a case for retaining easy policy settings.

That is more so with the growth outlook staying robust, despite poor rains. Exports have held up very well, with goods exports rising 16% year on year in April-June despite a sharp hit to shipments to GCC countries. Domestic activity indicators, including auto sales, GST collections and banking sector credit growth, have also been very strong. Credit growth, particularly, has been accelerating rapidly (18.6% year on year) and remains well above expected nominal GDP growth, therefore requiring vigilance. That is a sign that monetary and credit conditions are benign.

The policymakers should realise that the earlier narrative that higher crude prices and supply constraints will damage growth acutely has not proved correct. There is scope to attach much bigger weight to rising inflation in this context. At least neutral monetary policy settings are warranted, and some policy normalisation will not hurt growth either.

Two, some MPC members have argued that soft core inflation, despite strong growth, is a sign that potential growth could be higher (maybe closer to 8% rather than the long-period average closer to 7%). Therefore, the case is made that the RBI shouldn’t tighten despite strong GDP growth. Such arguments are not relevant here, however, given that policy settings need to be at least neutral currently. In fact, technically, stronger potential growth merits a higher neutral policy rate also.

Three, linked to the above discussion, RBI MPC shouldn’t allow real policy rates to dip into the negative zone, ex post or ex ante. But that is likely in the second half of the fiscal year at the current level of policy rates. Recall that, based on core inflation, the RBI ensured real policy rates of close to 2% in the pre-COVID period, when growth was 6.5-7%. A repo rate of close to 6% also looks suitable in the current backdrop. Negative real policy rates may be acceptable if growth is very weak or if inflation is very high but expected to come down. That is not the situation currently.

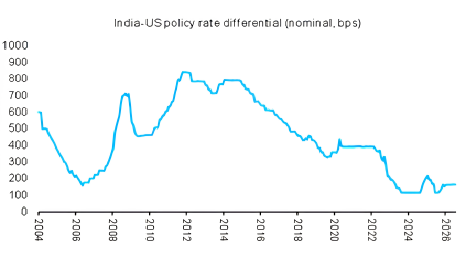

Finally, current policy rate settings also appear low in the context of the global interest rate trajectory. Interest rate differentials with the US appear too low, not just on a nominal but also on a real basis. If we conservatively assume that US underlying inflation is closer to 3% versus India’s 4%, then the current level of real policy rate differential is barely positive. As the US Fed has turned hawkish and has revealed a low bar for rate hike(s), there is additional risk of interest rate differentials narrowing further.

Chart: India-US interest rate differentials remain very low

As the rupee continues to trade near lows despite the RBI’s and the government’s bazooka announcements to attract flows, there is no scope for the MPC to be complacent. Note here that even as portfolio debt flows have improved recently, that may well be tactical. Also, from a rupee demand-supply perspective, the big elephant in the room is the relative demand-supply from exporters and importers. That, in turn, is a function of sentiment and hedge costs, which again mirror interest differentials.

RBI shouldn’t get caught in the narrative that interest rates and rupee outlook are completely delinked. There is a good case to believe equilibrium repo rate settings are higher than current levels. In the upcoming August MPC meeting, the communication/forecasts should continue to be tailored in a way to indicate that rate hike(s) remain firmly on the table in later meetings, despite a dip in crude prices.

More From BasisPoint