.png)

Sharmila Chavaly, a former civil servant who held key roles in the railways and finance ministries, specialises in infrastructure, project finance, and PPPs.

April 4, 2026 at 7:13 AM IST

China, the world’s largest importer of oil and gas, has so far weathered the shock to global energy markets from the war in Iran with surprising resilience. It holds reserves of 1.4 billion barrels, has a grid that integrates renewables at scale, and has an industrial policy that has made it the world’s leading exporter of solar panels, batteries, and electric vehicles. Much of Asia is now trying to adopt this strategy, as energy security means reducing dependence on seaborne fossil fuels through electrification, storage, and building of systems, not just by buying and storing fuel.

Where does India stand in this picture? We have already established that the recent gas pipeline push is just doubling down on a strategy prepared in the mid-2000s. The energy scenario was different then, and the infrastructure being laid today risks becoming stranded in the medium term. In parallel, there is a huge backlog in the renewables sector as systems for offtake and transmission have not kept pace with increased generation capability.

The issue, then, is not whether to build — India must build — but what to build, and where our scarce capital should go. Every rupee spent on pipelines is a rupee not spent on the grid, on storage, on the systems that will define India’s energy future. The choice is between locking into a specific fuel or building a system that can adapt to whatever comes next.

What is Electrostate

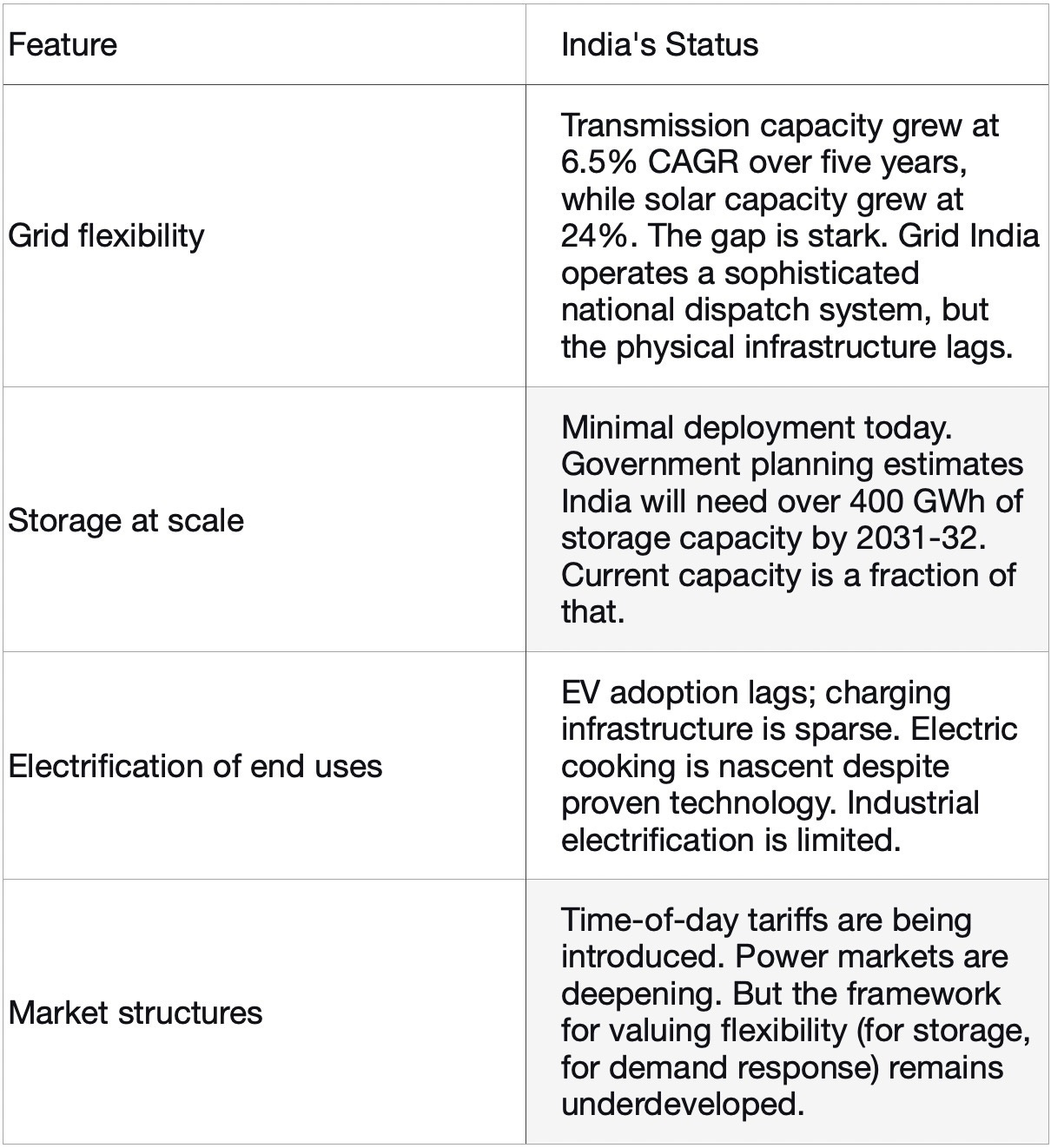

An electrostate has four essential elements.

First, a grid built for flexibility. The grid must be able to move power from where it is generated to where it is needed, in real time. This means transmission lines that connect renewable-rich regions to demand centres, and a national market that allows electrons to flow across state borders without friction.

Second, storage at scale. Renewables are variable. The sun does not always shine; the wind does not always blow. Storage - battery energy storage systems, pumped hydro, and emerging technologies - smooths out this variability, storing power when it is abundant and releasing it when it is needed.

Third, electrification of end uses. Transport, cooking, industrial heat - sectors that today run on imported oil, gas, and coal - must shift to electricity. Every electric vehicle on the road reduces demand for imported fuel. Every induction stove replaces LPG with domestically generated power.

Fourth, market structures that reward flexibility. The institutions of the electrostate, i.e., the pricing mechanisms, the contract frameworks, the dispatch rules, must be designed to value the ability to ramp up and down, to store and release, to shift demand to hours when power is abundant.

Where does India stand on each?

India is not on the path to becoming an electrostate because of a stated policy, but there are stray component elements that have been emerging in patches. There has been extraordinary progress in generation - over 265 GW of non-fossil capacity, 140 GW of solar, and a target of 500 GW by 2030. But generation alone does not make an electrostate. The systems that use that generation - the grid, the storage, the market structures - have not kept pace.

What China Did

China’s energy policy is built on energy security (reducing dependence on seaborne fossil fuels), domestic air quality (moving industry away from cities, replacing coal heating with gas), and technological leadership (dominating solar, batteries, and EVs as export industries). This is not a decarbonization strategy but a national security strategy; that it also reduces emissions is incidental.

The results are visible. China’s grid modernisation investment exceeded $85 billion in 2024. It built 41 ultra-high voltage “power highways” to move electrons from the resource-rich west to the demand-heavy east. Its battery manufacturing capacity is the largest in the world and its EV adoption rates are the highest. And crucially, it has systematically planned this, with 10-year anticipation roadmaps that align industrial policy, grid investment, and market reform.

In February 2026, China announced the next phase: dismantling provincial power protectionism to create a unified national power market. By 2030, the fragmented provincial markets that have long constrained its grid will be replaced with an open national energy market, and by 2035, full integration.

Yet the strategy is now straining under its own success. Renewable generation has grown so fast - solar capacity grew at a 24% CAGR - that it has begun to outpace even China’s massive grid expansion. The result is that by 2025, wind curtailment had risen to 6.6% and solar to 5.7%. In the second half of 2025 alone, over 10 GW of wind and solar projects were cancelled across six provinces because the grid could not physically connect them, leading to negative power prices in some regions.

Even the rollout of wires is getting stuck, with reports that available corridor resources have become scarce due to land disputes and environmental red tape. The lag between building a solar farm (12-18 months) and a major transmission line (36-60 months) creates a persistent bottleneck. China has quietly raised its official curtailment tolerance to 10%, up from 5%, because it is becoming impossible to integrate all the power.

The contrast with India remains instructive, but not in the way often assumed. India’s solar capacity grew at 24% CAGR over five years; its transmission capacity grew at just 6.5%. China built the wires alongside generation at a scale India has not matched. But China is now wrestling with the same transmission crises - curtailment, cancellations, negative prices - at a far larger scale. The lesson for India is not that China solved the problem but that building generation without the flexible grid to support it leads to the same outcome everywhere.

However, there is a crucial difference - what can be fixed, and what cannot. China’s problem is a coordination failure between generation and transmission. It can be fixed by building more wires and more storage. The investments required are large, but the path forward is clear. India’s gas pipeline lock-in is a fuel-specific problem. A pipeline built for gas cannot carry solar electrons. It cannot be retrofitted for flexibility. It is an irreversible commitment to a molecule. China’s grid constraints are reversible with investment, India’s pipeline assets, once sunk, are not.

China treated the grid as strategic infrastructure, to be built ahead of demand - and still fell behind. India treated it as an afterthought, to be expanded reactively. The result is visible in the 45-55 GW of renewable capacity in India waiting for signed PPAs, and in the 2.3 TWh of solar curtailed in just a few months of 2025, enough to power 400,000 households for a year.

This is not a matter of capability but one of strategy. If India follows the same path as China, it must avoid China’s current trap of building generation faster than the system can absorb. But it must also avoid its own trap, of locking itself into a fuel that the world is moving past.

Agnostic to Source

A grid built for flexibility can carry power from coal plants today and from solar farms tomorrow. It can integrate nuclear when it comes online, and storage when it scales. It can absorb power from rooftop solar panels on a million homes. It does not require betting on a single fuel, a single supply chain, a single set of import routes.

The electrostate is not a purity test. In the short run, countries under energy stress are turning to what works: coal plants running harder, restarting nuclear reactors, proliferating renewable generation projects, imposing energy use restrictions. Taiwan is restarting nuclear plants shut down last year. Vietnam is converting planned LNG projects to solar-plus-battery. Sri Lanka is rushing forward solar and hydro projects.

India will do the same. Coal will remain significant for years while nuclear will scale slowly. The question is not whether these sources exist, but whether the system can integrate them. A grid built for flexibility can absorb coal today and solar tomorrow, while a gas pipeline built today can only carry gas.

Strategic reserves vs. fixed infrastructure. China’s resilience comes not just from electrification, but from building up oil reserves over years. These are flexible and can be drawn down or built up as prices and geopolitics shift. A Morgan Stanley report had noted that stockpiling “behaves like incremental demand: persistent buying on dips, greater willingness to pay for security of supply.” That is a cost, but it is a manageable cost. Stranded pipeline assets are not. A gas pipeline cannot be drawn down, it is a fixed bet on a flow through a specific chokepoint, for a specific duration.

Even domestic coal benefits from the electrostate framework. Coal plants in India today are inflexible; they must run at minimum loads that constrain renewable integration. In an electrostate, coal would shift to a supporting role - ramping down when solar is abundant, ramping up when it is not. This is not an argument for coal expansion but an argument for building a system that can integrate whatever generation mix India chooses, rather than locking in a specific fuel.

The Storage Imperative

India’s storage requirements are now well understood. The Central Electricity Authority projects a BESS requirement of 47.24 GW by 2031-32, with other estimates going even higher: 50 GW by 2030, 116.9 GWh by 2050. The government’s own planning suggests over 400 GWh of total storage capacity will be needed by 2031-32.

The International Energy Agency projects India may become the world’s third-largest market for utility-scale batteries by 2030.

The good news is that costs are falling. Battery storage costs in grid-scale tenders have decreased by approximately 80% between 2022 and 2025. Solar PV plus battery storage is already cost-competitive with new coal-fired power. The policy framework has been catching up. The government has mandated that wind and solar PV projects incorporate at least 5% storage. In March 2026, a private party announced an investment of approximately ₹40 billion for a BESS plant in Haryana.

Across the world, too, energy storage is moving from pilot projects to industrial-scale deployment. Global battery cell shipments are projected to reach 801 GWh in 2026, with installations hitting 353 GWh. And emerging economies like Brazil, South Africa, and Vietnam have been accelerating apace with established leaders like the US and Australia. In fact, Brazil has formally recognized storage as an independent asset class with its own tariff and tax framework. Elsewhere, Romania is building storage capacity as “national resilience infrastructure.”

Each of these markets faces its own constraints, but the common thread is institutional innovation: clear revenue models, grid connection frameworks, and market structures that value flexibility. India has the generation capacity and now needs the storage, and the market frameworks, to deploy it at scale.

The Distributed Alternative

Uttar Pradesh has demonstrated what is possible. The state has achieved a cumulative installed rooftop solar capacity of over 1,190 MW, generating nearly 5 million units of carbon-free electricity daily. These systems have helped residents save over ₹320 million in electricity costs daily and have created direct employment for around 50,000 people. In a significant policy shift, the state government has made rooftop solar systems mandatory for approval of new residential building plans. Some other states are reportedly taking a cue from this.

This is distributed generation at scale. It bypasses the transmission bottlenecks that constrain utility-scale renewables and reduces the burden on discoms. It makes each household a producer, not just a consumer.

The same logic applies to electrification of end uses such as stoves, gas boilers, and vehicles, with each substitution reducing import dependence and strengthening the case for the electrostate.

Brazil offers a parallel lesson. Brazilian drivers can choose between 100% sugarcane ethanol and a gasoline blend containing 30% biofuel (the cars are dual use). The program, launched in 1975, has become a unique buffer against oil shocks. As the Iran war entered its fifth week, Brazilian gasoline prices rose just 5% in March, compared to 30% in the United States.

India has already begun down this path. The ethanol blending programme has reduced crude import dependence, with petrol now blended at around 20% ethanol in several regions (in Part 1 we had also discussed the proposal to extend ethanol to cooking fuel.) The Brazilian example shows what is possible when ethanol is integrated into the transport system at scale - not as a niche, but as a structural buffer. India’s electrostate does not have to choose between electrons and molecules but can build both, as long as the molecules are domestic and the electrons are clean.

The Data Centre Question

The government’s path is grid-first. Officials point to India’s unified national grid of 520 GW as a structural advantage. Captive generation is permitted but not required. Data centres would draw power like any other industrial consumer, with grid upgrade costs socialised across all users.

The concern is that allowing data centres to draw from the public grid amounts to cross-subsidy: residential and industrial consumers bear the cost of grid upgrades while Big Tech captures the profit. Proponents argue that large data centres should generate or procure their own clean power, without burdening retail consumers, some of whom already cope with load-shedding.

Maharashtra has taken a middle path. The state, which hosts nearly 60 per cent of India’s data centre capacity, allows data centres to set up captive renewable generation. Operators can apply for parallel distribution licences. Surplus power can be sold within the zone. This is not a mandate but an enablement.

The dependency risk cuts both ways. China’s dominance in solar panels, batteries, and EVs means that rapid electrification risks trading one form of dependency for another. The new BESS plant in Haryana is a start, but India needs strategic domestic manufacturing to ensure the electrostate is powered by Indian technology, not just Chinese exports.

The data centre question is a test case for the electrostate. If the grid is a commons, new load must either pay its way or be required to build its own capacity. While Maharashtra’s middle path is a start, the deeper question - who bears the cost of the transition - will persist. The answer will shape not just India’s data centre industry, but the architecture of the electrostate itself.

The Window

The window for this bet is open, but not indefinitely.

Transmission corridors are being planned. Storage costs are falling. Rooftop solar is scaling. The technology exists. The capital, much of it private, exists and is waiting for regulatory clarity. What is missing is not feasibility, but follow-through.

Every month of delay in transmission build-out pushes the renewables backlog deeper. Every discom that remains unreformed adds to the inertia that must eventually be overcome. Every rupee spent on gas pipelines is a rupee not spent on the grid, on storage, on the systems that define the electrostate.

The window will not stay open forever. The electrostate is being built, unevenly and incompletely, in parts of India today. Whether India seizes the crisis to accelerate that build-out or lets the window close will determine its energy future for decades.

This is Part 2 of a three-part series titled Why Waste a Good Crisis: India's Chance to Become an Electrostate

Part 1 covered India ‘s pipeline paradox — Speeding up gas pipelines risks locking India into a 20th century energy model, even as renewable capacity waits for transmission and PPAs.

Part 3 of this series will ask the harder question: given the institutional constraints, the fiscal pressures, and the political economy of incumbent interests, is India capable of making that transition?

More From BasisPoint