The propensity of Indians to hold gold is well known. It is held as an asset, a store of value, a token of auspiciousness and a status symbol. Together with China, the two countries account for over half the gold consumption in the world and with limited domestic production, gold also occupies a key place in India’s import basket.

As the West Asia crisis pressurised the rupee and India’s forex reserves, Prime Minister Narendra Modi’s recent appeal to Indians to voluntarily avoid buying non-essential gold and jewellery for at least one year might hold merit. What remains to be seen, though, is whether this appeal will attract the attention of the average Indian.

Suggestions to put off gold purchases by the government were followed by a hike in import duty on gold imports and may be a step in the right earnest as the country faces huge current account deficit and a falling rupee. However, this might not really make a large dent in lowering demand for the precious metal. Data suggests that demand may, in fact, remain elevated as SGB mature and redemptions lead to physical demand for gold, which may keep the import bill high.

Gold has always been a favoured investment product for Indian households, cutting across financial and social status. It has often been argued to be an unproductive instrument as it moves out of the economy and into the household and for a capital-intensive economy like India, it may not be the right investment. Thus, several government initiatives were introduced to reduce the physical demand of gold:

1) ETFs were launched in 2007, and gave investors the opportunity to buy gold in the demat form like a Mutual Fund unit. An investor has the option to redeem the units at any point in time and can convert it to physical gold whenever the need arises. A large benefit was the denomination - an investor could invest as low as Rs 100 to buy a gold ETF, and they do not need to worry about safekeeping of the gold.

2) Sovereign Gold Bond scheme was launched in 2014 and allows an investor to buy a gold bond at current prices and hold the same for a period of 8 years. At the end of this period, they would get the equivalent gold values at the current price. During this period, the investor also gets 2.5% annual interest on the investment. This scheme has been discontinued in February 2024.

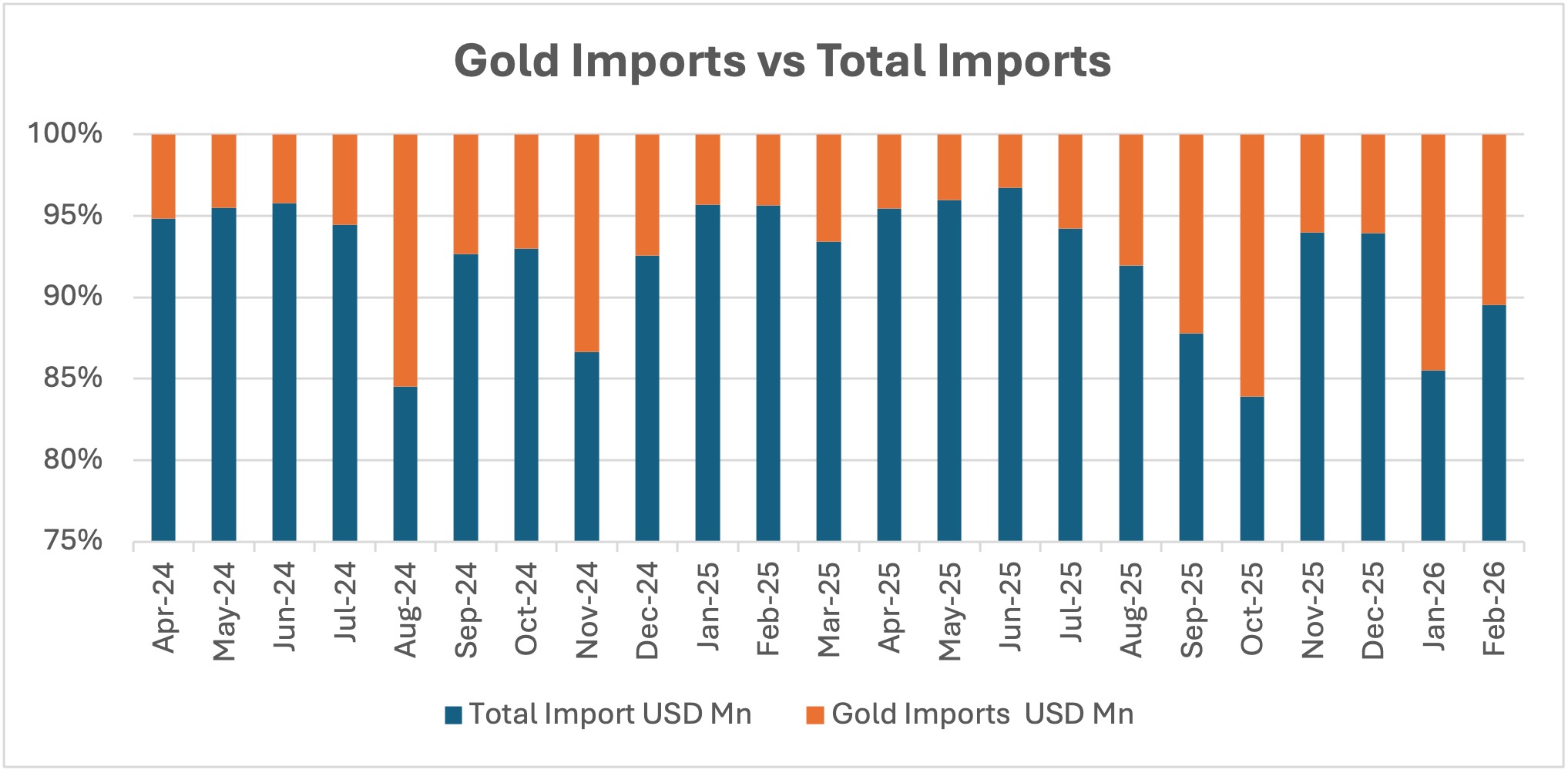

Both schemes postpone current demand to a future date. In the case of SGB, at maturity, a part of the total amount may be converted to physical gold as this is the nature of the product. This demand is in addition to the normal physical demand and would lead to increased gold imports. Accordingly, normal gold import comprises 5-6% of the import basket, but this number spikes around the time of maturity of the SGB, as seen in August 2024, September 2024 and October 2024. A similar uptick in gold imports was also seen in October 2025, November 2025, December 2025 and January 2026. (Chart 1). For reference, India’s annual gold imports stand at 700-800 tonnes a year, while the total outstanding SGB volume is around 124 tonnes.

(source: - DGFT trade statistics, HS Code 7108)

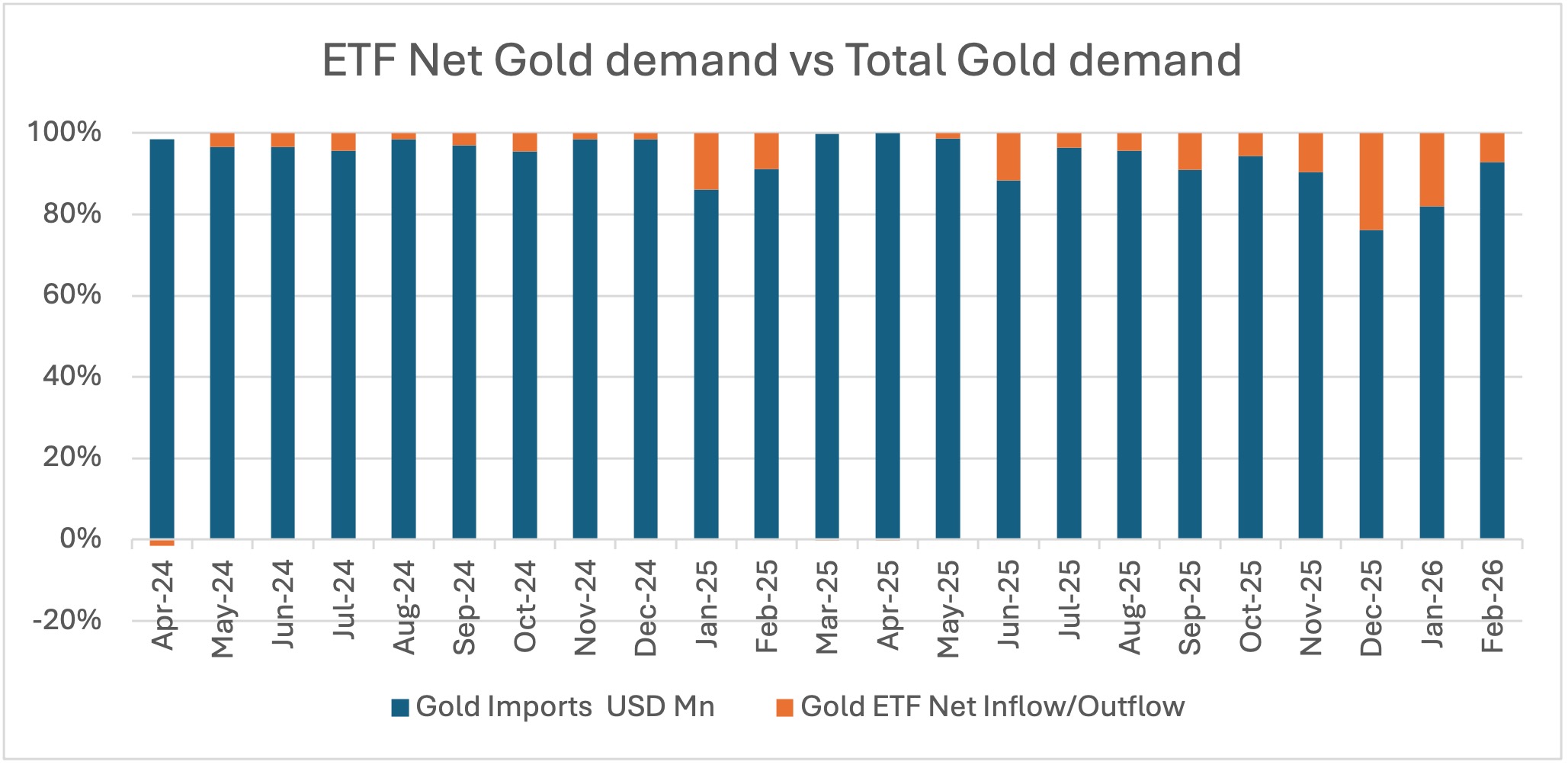

When it comes to gold ETF flows, during normal times the share of ETF gold imports versus total gold demand is 4-5%. However, in the months when gold prices have spiked, the share of ETF gold imports versus total gold imports has risen 10.48% (November 2025), 31.22% (December 2025) and 21.91% (January 2025). (Chart 2)

(source: - AMFI monthly/quarterly data)

Demand for physical gold by households looks to be steady, irrespective of the price of gold, and hence may not be speculative in nature. Sudden spikes in price may, thus, be related to maturity of gold bonds and since the government has already discontinued fresh issuances of these bonds, this demand may stabilise once all these bonds mature.

ETF flows, however, are more speculative and may continue to impact demand as and when there is volatility in gold prices.

* Views are personal

.png)