.png)

Phynix is a seasoned journalist who revels in playful, unconventional narration, blending quirky storytelling with measured, precise editing. Her work embodies a dual mastery of creative flair and steadfast rigor.

February 3, 2026 at 2:14 AM IST

Dear Insighter,

Have you heard the Kishore Kumar song Zindagi ek safar hai suhana, yaha kal kya ho kisne jaana? It’s a good reminder that hanging on too tightly is often pointless, especially when the plot keeps changing mid-scene. German author Hermann Hesse romanticised the idea of letting go, that true strength lies in surrendering control. But he probably never watched markets for a living. Here, “strength” usually means staying glued to your screen while the headlines refuse to slow down.

For months, data trickled in, forecasts nudged up or down, and everyone kept asking the same questions: what will break the range, when will the next trigger arrive, and is the US trade deal happening soon? Indian equity markets were also shrugging off major geopolitical events to stay largely listless, making investors nervous. Not much happened. Until suddenly, everything did.

This week arrived like one of those Ekta Kapoor episodes where five things happen in five minutes (a death, a reincarnation, a supernatural presence, and massive time jumps) and you still feel like it lasted forever. It felt longer than all of January put together.

There’s a fancy term for it: temporal distortion. Time seems to stretch when too much happens at once.

A fiscal blueprint that spooked markets for less than a day — on a Sunday, no less — followed by a near-midnight trade announcement that seemed to come from a universe where deals are declared while the rest of the world sleeps.

Let’s start with the Budget, the grand Sunday spectacle that had many of us postponing our birdwatching, as Kalyan Ram wistfully noted. Expectations were sky-high for a classic tightrope act. As Amitabh Tiwari had outlined in the run-up, the Finance Minister faced a formidable balancing exercise: immediate political compulsions with five states heading to polls, long-term fiscal credibility, rural stress, employment anxieties, and a middle class quietly hoping for relief.

What we got instead was a masterclass in what happens when you spend a long Sunday tracking schemes instead of sparrows. The speech was rich in coconuts, corridors and kartavya. But as Dhananjay Sinha put it neatly, it ultimately “settled for stability, not momentum”. The Budget walked the tightrope by refusing to dance on it at all.

The arithmetic offered little comfort to bond investors, notes Yield Scribe. Higher borrowing, sticky interest costs and no clear backstop for supply pressures left the market feeling like it had trained for a sprint and been handed a marathon with ankle weights. The 10-year benchmark’s nervous drift towards 6.85% isn’t just a number; it’s a sigh. Yet, as Chokkalingam G argues, was the nearly 2% equity sell-off a fair verdict? Probably not.

Given the pressure on tax revenues, the government stuck to its deficit targets with admirable discipline. But as Rajesh Mahapatra dissected, this discipline came from cutting transfers and development spending where it hurts most, effectively shifting fiscal stress to the states. Net tax collections fell short, cushioned by a hefty RBI dividend and ambitious disinvestment assumptions. Credible, yes, but also politically convenient.

The prevailing mood, as Madhavi Arora described it, was “deliberately uneventful”. A “chain-linked Budget”, in Yuvika Singhal’s framing: continuity over spectacle, institutional stability over fireworks. N R Bhanumurthy saw it as fiscally prudent and reform-oriented, another carriage on the reform express. And yet, a quiet question lingered beneath the calm: in a world tilting on its axis, is steady-as-she-goes enough?

The real story, as Vijay Chauhan reminds us, may not be the STT hike that briefly hijacked headlines and sank portfolios, but the fine print of extended filing timelines, simplified compliance, a deeper push towards trust-based execution. This is a document for builders, not traders; for patience, not adrenaline.

Then, just as the dust from the Budget began to settle, the ground shifted elsewhere.

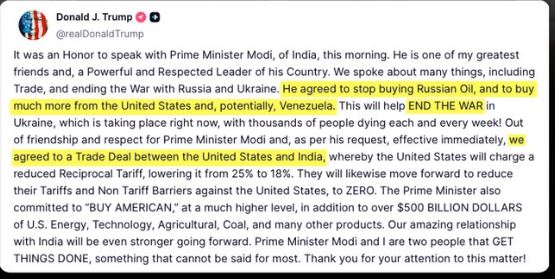

A US–India trade arrangement? US President Donald Trump declaring victory on Truth Social. Ambassador Gor “thrilled”. Prime Minister Narendra Modi thanking the Trump for tariff reductions, but conspicuously silent on oil purchases, commitment numbers or timelines. Declarative enthusiasm much? Well, markets and commentators will of course parse what was announced versus what was actually agreed.

At home, we are meticulously laying corridors and planting coconut saplings for 2047. Abroad, the weather changes with a phone call and a post. Indian exporters, as Rajesh Mahapatra highlighted in his pre-Budget conversation with EEPC’s Pankaj Chadha, have been clinging to hopes of trade relief amid tariff threats and weak global demand. The sudden shadow of a deal, details still emerging, throws a stark contrast on our domestic debates.

It raises the question the Economic Survey hinted at and Yuvika Singhal underlined: in a fragmented global order, can India pivot decisively enough to generate the export earnings and investor interest required to fund its ambitions?

Look closely and the Budget does send sharper signals than its calm surface suggests. The government is putting real money behind capex and expects corporate India to follow. Krishnadevan V decoded the hike in buyback taxation as a blunt “capex-or-consequences” message to promoters. If the state is shouldering the burden of infrastructure investment, surplus corporate cash should expand capacity, not flow back into promoter hands.

Similarly, Ajay Shankar’s warning to move beyond the “paracetamol” of PLI schemes remains pressing. Structural ailments like high energy costs, GST on fuels, and inefficient logistics continue to sap manufacturing competitiveness. The Budget gestured at reform, but the stronger medicine is still brewing.

Future-facing challenges received thoughtful, if cautious, attention. Kunal Tyagi rightly noted that the Budget cannot outspend Big Tech on AI compute, but it can shape demand and lower adoption barriers through procurement and standards. Venkatakrishnan Srinivasan flagged that India’s green bond programme sits at a crossroads, struggling to scale without clearer incentives. Arvind Mayaram made a compelling case for fixing carbon markets by funding public measurement and aggregation so farmers aren’t systematically excluded.

Sitting with it all, I’m reminded that the quiet months weren’t empty; they were loading stress. This week, the plates shifted. The Budget was one tectonic move, measured in basis points and borrowing numbers. The trade announcement was another, different in scale and tone, but just as disorienting.

Looking outward could help. Michael Debabrata Patra’s point about emerging markets sticking it out feels timely. They don’t behave like they used to. They bend more, panic less. Audentes fortuna iuvat — fortune favours the bold — but not the chest-thumping kind. This is a slower boldness. Staying the course. Negotiating without rushing. Building through the noise rather than reacting to it.

That’s probably why the week felt so long. It wasn’t just busy. It asked us to hold two opposing ideas at the same time. The careful, spreadsheet-heavy work of planning. And the sudden, headline-driven surprises that ignore all of it. Holding both without dropping either is exhausting. But it’s also, increasingly, the job.

Until next time, making sense of opposing ideas with strong coffee, and the faint hope that a free weekend is still waiting somewhere on the calendar.

Phynix

Also Read:

- Future to be Authored, Not Avoided by Probabilistic Pessimism by V Thiagarajan: A critique arguing that over-quantifying global risks can paralyse proactive policy-making into mere risk mitigation.

- Currency Valuation: From Competitiveness to Coping Mechanisms by R. Gurumurthy: Explores why currency valuation models often explain market discomfort better than they predict actual exchange rate movements.

- Gold Fantasies vs. Financial Reality: The Reserve Narrative That Doesn’t Add Up by R. Gurumurthy: Why narratives of gold reclaiming monetary dominance ignore modern financial system constraints and operational realities.

- The Turkey Illusion by V Thiagarajan: How the illusion of rupee stability in 2024 masked underlying risks that eventually erupted into volatility.

- India Lowers Import Barriers Where It Matters Most by Ajay Srivastava: How the Union Budget, while country-neutral, strategically improves market access for key US exports.

- India-EU Trade Deal: Beyond the Headlines by Rajesh Mahapatra: A deep dive with a former negotiator into the fine print and implementation challenges of the India-EU free trade agreement.

- Spaghetti Bowl: You Have Been Served by Reform Compass: The paradox of how India could have better used market access to boost FDI and domestic manufacturing.

- The Great Global Repurposing of IPOs by Candrika Soyantar: Global IPO markets are now segmented, funding national priorities like defence and frontier tech over pure growth stories.

- Spotlight Back on Process Patents by TK Arun: The rise of personalised medicines necessitates urgent changes in India's approach to drug trials, patents, and regulation.

- Govt for High Level Banking Panel, The Real Question Is Why Now by Mint Owl: Questioning the rationale for a new banking committee when the system appears stable, profitable, and already reforming.

- When Disclosure Meets Discipline: Recasting India’s Financial Regulatory Architecture by Srinath Sridharan: Calls for an integrated approach to systemic risk, moving beyond the current divide between disclosure and prudential regulation.

- Tax Residency Certificates No Longer Sacred After Supreme Court's Tiger Global Verdict by Sangeeta Jain: A landmark Supreme Court ruling that weakens treaty protections for offshore investors and empowers tax authorities.

- High Lapse Rate of Life Insurance Policies in India and Why It Matters by Alpana Killawala: The widespread lapse of life insurance policies and the significant financial protection lost as a result.

- Why Fight for Oil When the Sun Shines Free? by Nilanjan Banik: A global shift to renewable energy could fundamentally reshape geopolitics and reduce conflicts linked to fossil fuels.

- Why Govt Should Hike Customs Duty on Gold, Vegetable Oils by G. Chandrashekhar: A case for higher import duties to curb a widening trade deficit, support the rupee, and protect farmers.

- Adani Green's Growth Machine Faces a Reckoning on Value by Dev Chandrasekhar: Questioning the premium valuation of India's renewable energy leader amid concerns over collapsing profits and high debt leverage.

- The Snack Boom Is India’s Tobacco Moment by Krishnadevan V: A parallel between investor fervour for snack brands and the tobacco industry, warning of mounting long-term health and regulatory risks.

- The Injection That Replaced Your Doctor With a Dose Chart by Krishnadevan V: The pharmaceutical industry's shift towards turning obesity treatment into a recurring revenue stream, potentially sidelining medical oversight.

- Fiscal Federalism, Transfers, and the Case for an Independent Anchor by Arvind Mayaram: Proposing an independent mechanism to restore trust and stability in India's fiscal transfer system amid growing discretion.

- Accountability as Publishers, Not Bans, Is the Solution to Social Media Harm by TK Arun: Advocating for holding social media platforms accountable as publishers rather than relying on hard-to-enforce age bans.

- Sarci-Sense: You’re Either Silent Or Unbearable. Neither Is Conversation. by Srinath Sridharan: A reflective piece on how modern communication has mastered noise and silence but lost the essential art of true conversation.

- A Postcard from Gandhi Ashram, Ahmedabad by Sudipta Sarangi: A personal and meditative visit to Sabarmati Ashram, reflecting on Gandhi's simplicity and enduring relevance in modern India.

- India’s Defence Budget: From Readiness To Endurance by Lt Gen Syed Ata Hasnain: Analysing the latest defence allocation, noting a strategic shift from funding short-term readiness to building long-term military endurance.

More From BasisPoint