.png)

Dhananjay Sinha, CEO and Co-Head of Institutional Equities at Systematix Group, has over 25 years of experience in macroeconomics, strategy, and equity research. A prolific writer, Dhananjay is known for his data-driven views on markets, sectors, and cycles.

February 14, 2026 at 5:13 AM IST

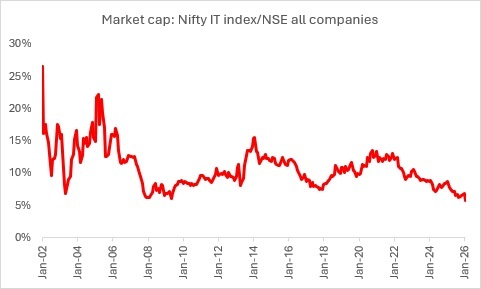

The NIFTY IT index has corrected sharply, declining 25% in recent months, including nearly 10% in a single month, wiping out more than ₹9 trillion in market capitalisation. One of India’s most globally integrated sectors has become a drag on benchmark indices, even as broader macro anxieties over US tariffs have eased.

The anticipated relief rally has bypassed technology stocks.

Foreign portfolio investors have pared exposure, unsettled by soft earnings guidance and valuations that no longer offer a growth premium. Domestic investors, who once chased technology momentum during mid-cap rallies, have turned cautious after repeated drawdowns. What had long been treated as a defensive compounder has abruptly been repriced as a cyclical and structural risk.

Commerce Minister Piyush Goyal’s intervention, urging investors to treat the correction as a buying opportunity, reflects confidence in the durability of India’s technology franchise. His vision, articulated at the launch of NITI Aayog’s Technology Services – Reimagination Ahead initiative, imagines the sector scaling towards $1 trillion by the mid-2030s, powered by applied artificial intelligence, hyperscale data centres, clean energy infrastructure, and indigenous 6G capabilities.

The question is whether policy optimism aligns with structural reality.

For three decades, Indian IT rode two durable waves: wage arbitrage and globalisation. As manufacturing gravitated towards China, enterprise services migrated to India. Firms such as Infosys, TCS and HCL Technologies built scale on offshore delivery models, predictable time-and-material contracts, and expanding US corporate technology budgets. In the five years ending 2007-08, sector market capitalisation compounded at roughly 55% annually.

That era appears to have faded.

Since the global financial crisis, Indian IT’s share of US technology market capitalisation has shrunk materially. The sector has remained profitable and cash generative, yet it has not meaningfully participated in the value creation seen in US platform companies. The gap reflects structural divergence.

India’s aggregate research and development spending remains below 1% of GDP, compared with roughly 2.5% in China and above 3% in the US. Private capital has favoured scalable services over deep technology risk. As frontier innovation shifted towards artificial intelligence, semiconductors, and advanced computing, Indian firms remained predominantly integrators rather than originators.

Model Disruption

Over the past 18–24 months, discretionary enterprise technology spending has slowed. Clients in banking, telecom, retail and technology have prioritised cost control, extended deal cycles, and renegotiated contracts. Earnings downgrades across large and mid-tier companies reflect that caution.

Artificial intelligence has transformed that cyclical slowdown into a structural pivot.

Large language models developed by OpenAI and Anthropic have begun automating meaningful portions of the software development lifecycle. Coding assistants and testing copilots are delivering measurable productivity gains, in some cases 30–50% improvements in developer throughput. Documentation, maintenance, and cloud migration workflows are increasingly automated.

This creates a tension at the heart of the Indian IT revenue model. Traditional contracts scaled with headcount. More engineers meant more billable hours and revenue visibility. AI compresses the effort required to deliver the same output. If a project requires fewer engineers and fewer hours, time-based billing naturally contracts.

The risk investors are pricing in is not margin collapse but revenue compression. Clients embedding AI into internal workflows may reduce outsourced volumes even as they seek advisory support. Mid-tier firms, with narrower client concentration and less consulting capability, face sharper exposure.

Yet the disruption is not unidirectional.

End of a Model

Enterprises adopting AI at scale require data modernisation, governance frameworks, cybersecurity safeguards, model integration, and domain customisation. Legacy-heavy environments, particularly in regulated sectors such as banking and telecom, cannot be overhauled by generic models alone. They require integration partners with execution depth and balance sheet credibility.

The opportunity set therefore shifts from labour arbitrage to outcome engineering. Pricing models are likely to evolve from effort-based contracts towards value-based or managed service structures. Growth rates may moderate from the hyper-expansion of earlier decades, but margins could remain resilient if productivity gains are captured rather than passed through entirely to clients.

The current market correction reflects uncertainty about that transition path. Investors are grappling with a simple question: will AI reduce aggregate demand for outsourced services, or will it expand the addressable market by accelerating digital transformation?

History offers partial guidance. Indian IT has previously adapted to shifts, from Y2K remediation to ERP implementation, from infrastructure management to cloud migration. Each wave required capability upgrades but preserved the sector’s relevance. The present shift is deeper because it questions the underlying revenue denominator, not just the technology stack.

This is not a sunset industry. It is an industry confronting the end of a comfortable model.

The wage arbitrage thesis that defined India’s outsourcing ascendancy is no longer sufficient. The next phase demands proprietary platforms, domain-specific AI tools, deeper consulting integration, and intellectual property creation. Firms that reposition as AI orchestration partners rather than labour providers can retain strategic importance.

The equity market correction, therefore, is less a verdict on extinction and more a repricing of transition risk. Some franchises will execute the pivot and consolidate share. Others may struggle as pricing power shifts and volume growth slows.

Whether this moment proves to be capitulation or opportunity depends not on policy exhortation but on corporate reinvention. The sector’s past was built on scale. Its future will depend on differentiation.

More From BasisPoint