Foreign portfolio investors pulled ₹1.18 trillion out of Indian equities in March. This is the largest single-month exit on record, eclipsing even the ₹940 billion that left in October 2024. In the same month, Indian mutual fund investors put ₹320.87 billion into the market through SIPs, an all-time high.

The familiar triggers are a hawkish US Fed, West Asian conflict squeezing oil supply lines, and a rupee under pressure. But the more convincing explanation is that foreign fund managers do not invest in rupees, but in dollars.

A 12% rupee return sounds attractive. After capital gains tax revisions introduced in the 2024 Union Budget, withholding tax on dividends, and factoring in rupee depreciation at repatriation, the dollar-adjusted, post-tax return competes poorly against other emerging markets bidding for the same allocation. In 2025-26 net FPI outflows hit nearly ₹1.8 trillion, up 42% year-on-year, the highest in 34 years. India needs foreign capital. This is not the column that argues otherwise. FPIs set the marginal price, anchor valuations to global risk norms, and provide the liquidity depth that domestic capital alone cannot replicate. The argument here is narrower. Build a domestic base strong enough that when foreign capital exits, and it will, repeatedly, the floor does not give way.

Ownership Shifts

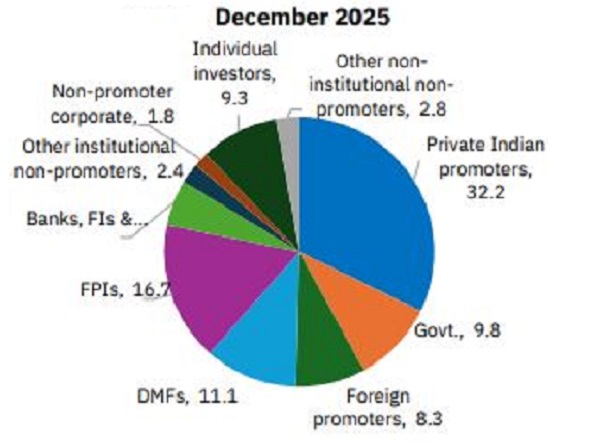

The National Stock Exchange of India’s data, as on December 2025, is unambiguous. Domestic mutual funds held 11.1% of all NSE-listed companies, the tenth straight quarterly record. Total DII ownership stood at 19%, ahead of FPIs for five consecutive quarters. FPI share slipped to 16.7% — a 15.5-year low. SEBI Chairman Tuhin Kanta Pandey confirmed in March 2026 that retail investors and mutual funds together hold 36% of Nifty 50 free-float market capitalisation.

NSE-listed universe: Ownership pattern by total market cap (%)

The rupee-value holdings of FPIs actually rose 4.6% quarter-on-quarter in October-December, even as their ownership share fell. Foreign capital is not abandoning India. It is concentrating with fewer positions, larger bets, and reduced breadth. Domestic mutual funds are doing the opposite, building ownership that is wide, compounding, and distributed across the listed universe. That breadth provides stability when external shocks arrive and concentrated foreign money moves fast.

Mutual funds have reached this position on the back of 97.2 million SIP accounts and ₹73.73 trillion in total AUM as of March 2026, with equity inflows in March alone hitting ₹404.5 billion. The firepower exists, but the question is how it is being used.

In March, mutual fund cash holdings fell to ₹1.86 trillion — a 16-month low — as fund houses reportedly deployed ₹243.19 billion into equities during the correction. Nearly 60% of funds actively bought during the drawdown. Cash as a percentage of AUM declined to 4.73%, from 5.76% a year ago. The question is whether it reflects structural accumulation or simply a mechanical response to low prices. That will indicate whether India's funds are building ownership with intent or by reflex.

Benchmark-tracking constraints and tracking-error penalties push fund managers toward index-hugging precisely when contrarian buying would be most valuable. The sectors FPIs have sold hardest — IT, financial services, large-cap consumer — are also the sectors with the most visible and durable underlying businesses. Buying them when foreigners exit for currency and tax reasons rather than business reasons is a valuation decision with a well-worn return profile.

Missing Pillar

Mutual fund flows are consistent but not unconditional and a sustained bear market could simultaneously trigger FPI exits and MF redemptions, thinning the domestic floor at the precise moment it needs to hold. India has no structural answer to that scenario today.

Australia's superannuation system mandates 12% employer contributions and has built a domestic equity base that absorbs selling without amplifying it. US pension funds hold trillions in domestic equities as capital that neither reprices geopolitical risk mid-quarter nor exits when withholding tax calculations turn unfavourable.

India's National Pension System manages ₹14 trillion-₹15 trillion, or roughly one-fifth of mutual fund AUM. The Employees’ Provident Fund Organisation allocates only a small portion of its far larger corpus to equities. Neither institution is scaled for the permanent, long-duration equity ownership the market needs as its third pillar.

SIP flows deliver consistency, but pension capital delivers permanence. The gap between those two things is most dangerous when FPIs and mutual fund investors are both heading for the exit simultaneously.

The January-March NSE Ownership Tracker, when published, will likely show domestic fund ownership crossing 11.5% and FPI share falling below 16% for the first time since the early 2010s.

The policy response to this need not be complicated. Make dollar-adjusted equity returns competitive through rational tax calibration, not as a favour to foreign investors but as basic maintenance of capital allocation efficiency.

Give EPFO and NPS a phased mandate to raise equity exposure meaningfully. Both steps together create a market with three load-bearing pillars instead of two.

If pension capital stays on the sidelines, the next simultaneous FPI and MF exit will be absorbed by a floor that cannot hold both.

(This column reflects the author’s personal views and is based on publicly available information. It is intended for general commentary and analytical purposes only and should not be construed as investment advice.)

.png)